It is a major player in the Indian life insurance sector with a market share of 66% of the total premiums. 1956 founded LIC, India’s largest asset management company. Till recently LIC was 100% government-controlled but now it has a 3.5% stake available to investors in Offer for Sale (OFS).

The interesting thing is that many of us do not want to become LIC shareholders – and that’s why today we bring you the complete fundamentals and competition analysis of LIC IPO – so that you have all the important numbers before investing.

Let’s see them one by one –

Angel shoutout

If you want to be the number 1 full-service broker in the country, which has just transformed into a fully functional FinTech company, open your Demat account with Angel One, and get access to great features like

- One-year Free AMC

- Small case

- SmartAPI

- Flat 20 Rs brokerage

- Personalized advisory

- MTF Facility

To take advantage of all, click on the link given in the description and open your free Demat account today.

First, we will look at the financials of LIC

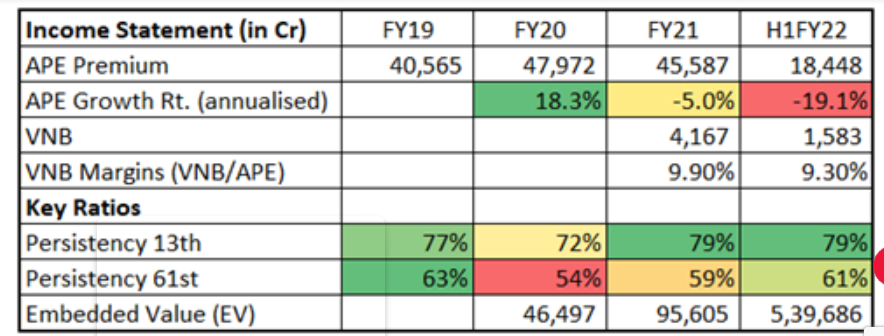

Above the table are some important financial data of LIC –

The embedded value of LIC is Rs. 956 billion to Rs.5.4 trillion by September 2021.

If you are wondering what is Embedded Value, then let me tell you that Embedded Value or EV is the sum of all future premiums to be received from existing policies. It can be taken as a definite component in evaluation.

Next, there is persistence – what is perseverance? Well, it is the ratio of the number of life insurance policies and net active policies receiving premiums on time in a year. Long term continuity ratio like 5 years is more important to understand whether a policyholder is continuing his policy or not.

A persistence ratio of 50% for the 5th year (or 61 months) means that only 50% of policyholders have continued to pay premiums, while the rest have discontinued.

LIC’s VNB margins FY21 and 1HFY22 are up against some 9.9% and 9.3% – largely reflecting a cross-heavy product mix.

Now you must be wondering what is VNB Margin? Well, VNB Margin is the sum of the future premiums of this year’s policies (using the same firmness and profit assumption). This is nothing but the EV for each year in the future.

According to DRHP, in the scenario of 10% surplus sharing in Par products, LIC’s FY21 VNB margin may increase to 12.3%, ceteris paribus. This compares to a 25%-26% comparable margin for listed industry peers.

Finally, Annual Premium Equivalent (APE) is a measure used to compare life insurance revenue by normalizing policy premiums to the equivalent of regular annual payments.

Basically, everything is pretty positive.

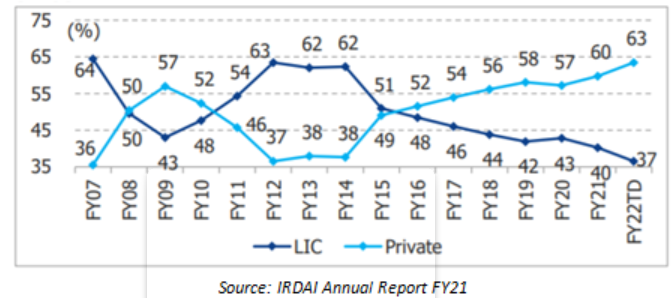

Unfortunately, LIC’s Retail APE market share has been falling since 2015 and has now fallen from 51% to 38%

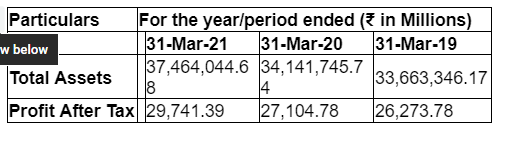

Income and profit-wise LIC has seen only growth, year after year –

There are also some special USPs of LIC –

LIC is the largest insurance company in India and the fifth-largest insurer in the world.

LIC has a range of life insurance products apart from personal needs, which have the power to fulfill all the insurance needs.

LIC has a strong omnichannel distribution network – 1.34 million agents, 3463 active micro insurance agents, and, 174 alternate channels

LIC is India’s largest asset manager but ISS company also has a good financial performance track record

Apart from this, the company also has a highly experienced and qualified management team.

LIC also has some challenges, such as –

Bad new policy growth – Day by day LIC is losing its market share, especially in urban areas.

Change in Embedded Value due to sharp fluctuations in interest rate,

high dedication

Valuation of LIC

Remember, insurance companies have a slightly different business model. Therefore, they do not report their financial statements like other companies. Therefore, do not consider ROEV, or P/E ratio type ratio, as a basis for analysis.

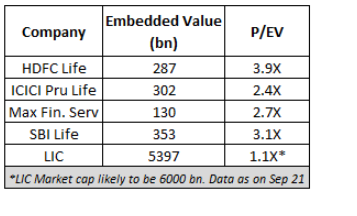

Insurance companies are valued as [EV + P/VNB or DCF of the value of new business]. The use of P/EV is not the correct way to value an insurance company, but it can only be used for reference versus other counterparties.

EV is the embedded value of the future premium this stream of cash flows is valuable to shareholders. Present Value of New Business which is nothing but EV from the future is added here. It gives the market capitalization for the company. This in turn is used by analysts calling it P/EV.

LIC is expected to be listed at a valuation of 1.1X Embedded Value, which is at a significant discount to its listed peers – so where LIC’s P/EV is 1.1X, the same currently listed players such as SBI Life, HDFC Life, And the average P/EV of ICICI Pru Life is some 2.5X

All-in-all is looking ever positive competition analysis wise too.

So should investors subscribe to LIC IPO or not?

All angles considered, policyholders, retail investors, and employees can subscribe to the IPO – but it is better if you are looking for a better fit for your portfolio – and no matter how small or large your overall portfolio – LIC Shares Position is just 5 %.

Keep in mind, retail individual investors can take LIC IPO A minimum of 1 lot (15 shares) – and a maximum of 14 lots –

So if you want to get 1 lot then your investment will be Rs. 14,235 and if you lie the maximum lot then your investment will be Rs. 1,99,290 would be.

If you want to subscribe to LIC IPO then –

Know when and what is the schedule for LIC IPO